Semico is a semiconductor marketing & consulting research company located in Phoenix, Arizona. We offer custom consulting, portfolio packages, individual market research studies and premier industry conferences.

There are challenges on the semiconductor supply side that will place some restraints on semiconductor sales in 2021. As electric vehicles and AI continue to penetrate the general consumer market, there are reports of chip shortages. Current semiconductor manufacturing capacity is finding it challenging to keep up with demand. A new report from Semico Research, Semico Wafer Demand Q1 2021 Highlights (MA110-21), forecasts wafer demand for 2021 to increase 8.2% in 2021.

The Wafer Demand Summary and Assumptions is a quarterly publication. It includes an excel spreadsheet with annual wafer demand by product by technology from 2010-2025. Product categories include DRAM, SRAM, NAND, NOR, Other Non-volatile, MPU, MCU, DSP, Computing MOS Logic, Communications MOS Logic, Consumer MOS Logic, Automotive MOS Logic, Other MOS Logic, Programmable Logic, Standard Cell, Gate Array, Analog, Discrete, Optoelectronics, Sensors and Digital Bipolar.

The semiconductor intellectual property (SIP) market is an integral part of the semiconductor industry. Third-party IP has propelled the industry, opening the door for many new products from start-ups to established IDMs. Enabling increasingly complex devices, reducing the cost of product development and reducing the time to market for both leading-edge and mature products are just a few of the benefits of third-party IP.

Semico Research conducted a survey in November 2020 of RISC-V users. This follows an initial survey and report published by Semico in 2019. With this study, we wanted to quantify the total available market (TAM) for IP cores and estimate the served available market (SAM) for RISC-V IP cores. We surveyed and interviewed a cross section of the semiconductor industry in order to gather information related to the type of devices that are being designed with RISC-V and their target markets.

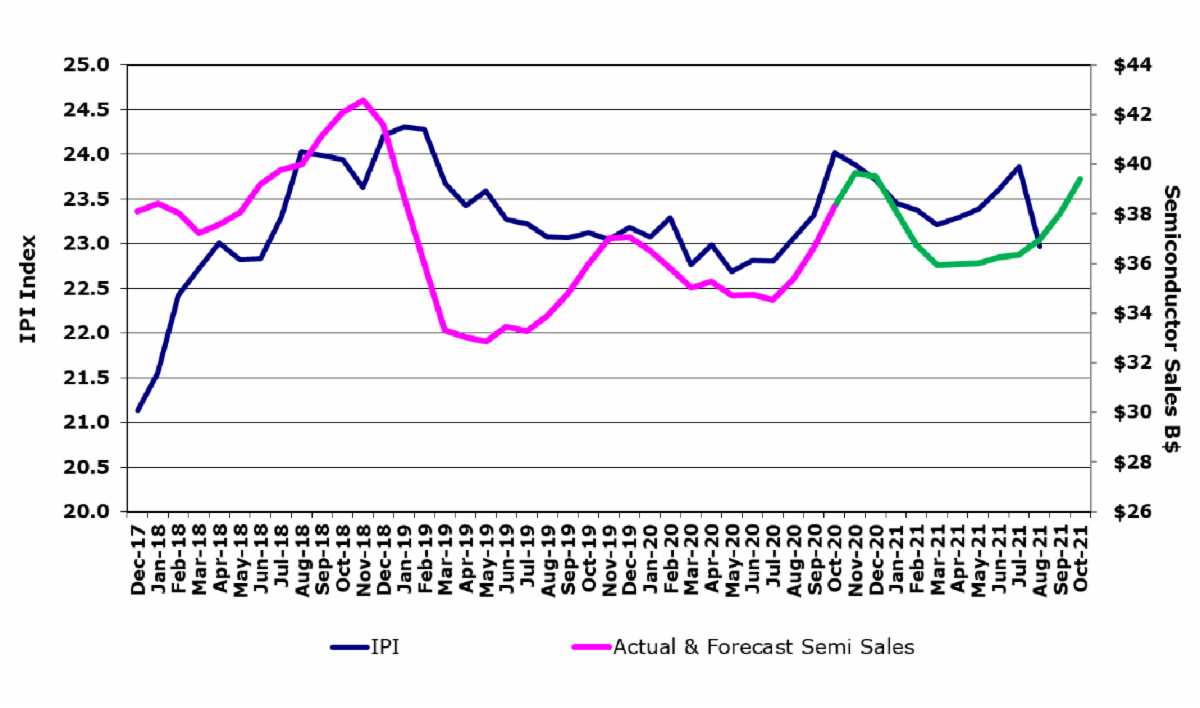

There is a significant amount of economic uncertainty due to the COVID‑19 pandemic; however, Semico’s outlook for semiconductor sales includes several areas of growth which have positively impacted the updated forecast. A new report from Semico Research, Semico Wafer Demand Q4 2020 Highlights (MA112-20), forecasts wafer demand to grow by 3.1% this year over 2019.

The Wafer Demand Summary and Assumptions is a quarterly publication. It includes an excel spreadsheet with annual wafer demand by product by technology from 2010-2024. Product categories include DRAM, SRAM, NAND, NOR, Other Non-volatile, MPU, MCU, DSP, Computing MOS Logic, Communications MOS Logic, Consumer MOS Logic, Automotive MOS Logic, Other MOS Logic, Programmable Logic, Standard Cell, Gate Array, Analog, Discrete, Optoelectronics, Sensors and Digital Bipolar.

Semiconductor revenues in September grew 11.4%, breaking a three-year streak of single-digit monthly increases. 3Q 2020 revenues grew 10.8% over 2Q 2020 and 6.4% over 3Q 2019. Semico is forecasting 4Q 2020 revenues will decline 0.4%; this will result in revenue growth for the year of 5.3%.

The semiconductor industry today is faced with several substantial issues—the continuing rise in design costs for complex SoCs, the decrease in the incidence of first-time-right designs and the increase in the design cycle time against shrinking market windows and decreasing product life cycles. An additional factor has now been added to SoC design costs with the emergence of complicated software applications intended to run on the SoC silicon. As happens often in our industry, the right solution surfaces at the right time.

The global electronics market is expected to consume over 160 billion Analog ICs in 2020. This translates to several Analog ICs per electronic device but is down 1.5% compared to 2019 unit sales. While Analog ICs are essential to electronic systems, this will mark the second year in which revenues and units both register declines. That has not happened before during the past 20 years.

To combat rising SoC design costs and increasingly complex software applications, a solution has been developed: the incorporation of AI functionality into existing EDA tools as an aid to silicon and software designers. A new report from Semico Research, Designing New Directions in the EDA Market: Designing with AI Tools (SC109-20) projects that cost savings from using AI EDA tools for SoC designs ranges from 20% to 30%.