Semico is a semiconductor marketing & consulting research company located in Phoenix, Arizona. We offer custom consulting, portfolio packages, individual market research studies and premier industry conferences.

published by Rich Wawrzyniak on Thu, 2020-07-23 21:37

On June 23rd, 2020, Siemens AG signed a letter of intent to acquire Cambridge, UK-based 3rd Party Semiconductor Intellectual Property (SIP) vendor, UltraSoC. Terms of the transaction were not disclosed except to say Siemens plans to integrate UltraSoC’s technology into the Xcelerator portfolio as part of Mentor’s Tessent™ software product suite. The acquisition is expected to close in Siemens 4th fiscal quarter this year.

There are several areas where this acquisition is impactful to the SIP market, the EDA market and the broader semiconductor market.

The Wafer Demand Summary and Assumptions is a quarterly publication. It includes an excel spreadsheet with annual wafer demand by product by technology from 2010-2024. Product categories include DRAM, SRAM, NAND, NOR, Other Non-volatile, MPU, MCU, DSP, Computing MOS Logic, Communications MOS Logic, Consumer MOS Logic, Automotive MOS Logic, Other MOS Logic, Programmable Logic, Standard Cell, Gate Array, Analog, Discrete, Optoelectronics, Sensors and Digital Bipolar.

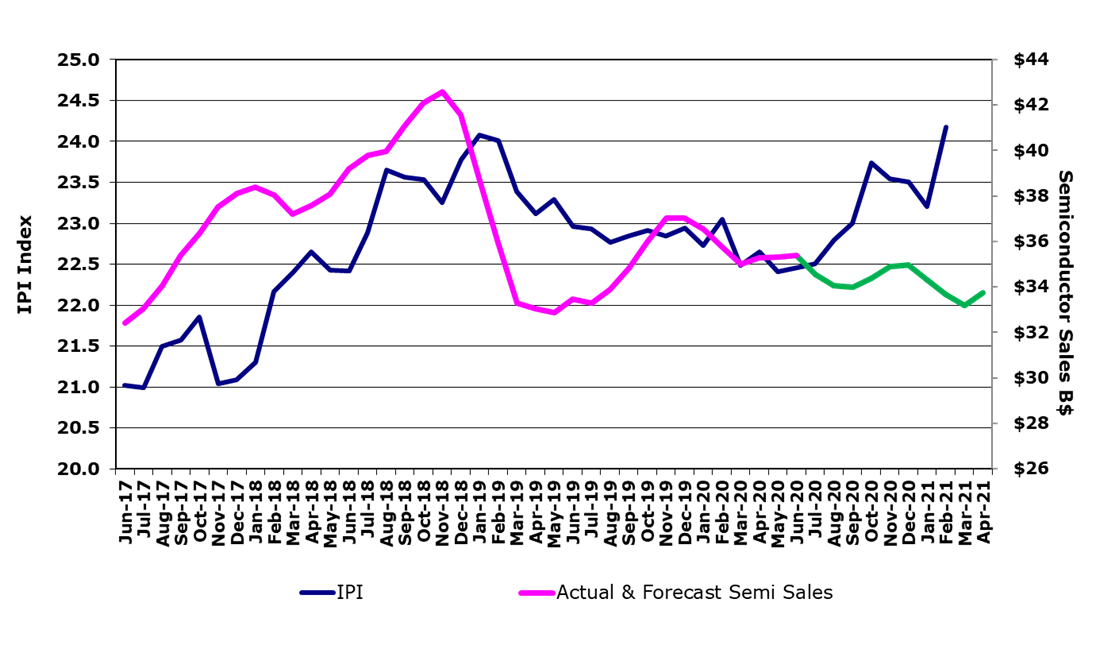

May 2020 semiconductor revenues increased 9.0% from April, which was down 14% from March. April's 14.2% drop was the largest sequential decline since 2011, but May's 9.0% increase was the largest for the month of May since 2006. Year-over-year, May was up 6.4% compared to May 2019. The North American PCB book-to-bill ratio fell from 1.19 in April to 1.1 in May. However, anything above one is a positive sign for sales six months out. The ratio has been at 1.0 or higher since May 2019.

Silicon Carbide (SiC) is a wide bandgap material and can be used for discrete components such as Schottky diodes and MOSFETs as well as bare die in power modules. Wide bandgap (WBG) refers to materials that permit devices to operate at much higher voltages, frequencies and temperatures than conventional semiconductor materials like silicon and gallium arsenide. It offers many advantages, including higher thermal conductivity that results in more efficient heat transfer and a lower on-state resistance that decreases conduction losses.

Silicon Carbide (SiC) is a wide bandgap material and can be used for discrete components such as Schottky diodes and MOSFETs as well as bare die in power modules. Wide bandgap (WBG) refers to materials that permit devices to operate at much higher voltages, frequencies and temperatures than conventional semiconductor materials like silicon and gallium arsenide. It offers many advantages, including higher thermal conductivity that results in more efficient heat transfer and a lower on-state resistance that decreases conduction losses.

The semiconductor industry today is faced with several substantial issues-not the least of which are the continuing rise in design costs for complex SoCs, the decrease in the incidence of first-time-right designs and the increase in the design cycle time against shrinking market windows.

The semiconductor industry today is faced with several substantial issues—not the least of which are the continuing rise in design costs for complex SoCs, the decrease in the incidence of first-time-right designs and the increase in the design cycle time against shrinking market windows.

Despite the pandemic disrupting life around the world in 1Q 2020, quarterly semiconductor revenues declined by only 3.4% from 4Q 2019 and were up 6.8% compared with 1Q 2019 revenues. However, part of that recovery is the fact that 1Q 2019 revenues were down -14.6%, a much higher decline than seasonally normal for a first quarter. Units fell -5.6% sequentially. Our overall 2020 revenue forecast has been lowered to slightly negative to -0.22%.

Today it is clear that the U.S. and world GDP will suffer due to the Covid-19 pandemic, and most forecasters are adjusting their numbers down. On the other hand, the semiconductor industry is experiencing a few sparks of positive demand by responding quickly to the warning signs from China and the shelter-at-home directive. Semiconductors used in sensing and monitoring medical end applications are expected to remain in high demand through 2020 and new wearable products are already being introduced.

The Wafer Demand Summary and Assumptions is a quarterly publication. It includes an excel spreadsheet with annual wafer demand by product by technology from 2010-2024. Product categories include DRAM, SRAM, NAND, NOR, Other Non-volatile, MPU, MCU, DSP, Computing MOS Logic, Communications MOS Logic, Consumer MOS Logic, Automotive MOS Logic, Other MOS Logic, Programmable Logic, Standard Cell, Gate Array, Analog, Discrete, Optoelectronics, Sensors and Digital Bipolar.