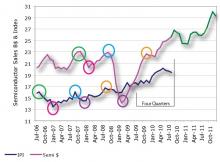

Phoenix, Arizona November 2, 2010 - It seems everywhere we turn, there is hype about how low 2011 will go. Our own opinion is that 2011 will be an above average growth year, rising 9.5% over 2010. Considering an average growth year for the semiconductor industry is 8% growth, 9.5% is pretty good.

Our forecast is based on our IPI (Inflection Point Indicator) which has been an accurate indicator of the industry's ups and downs for 15 years.